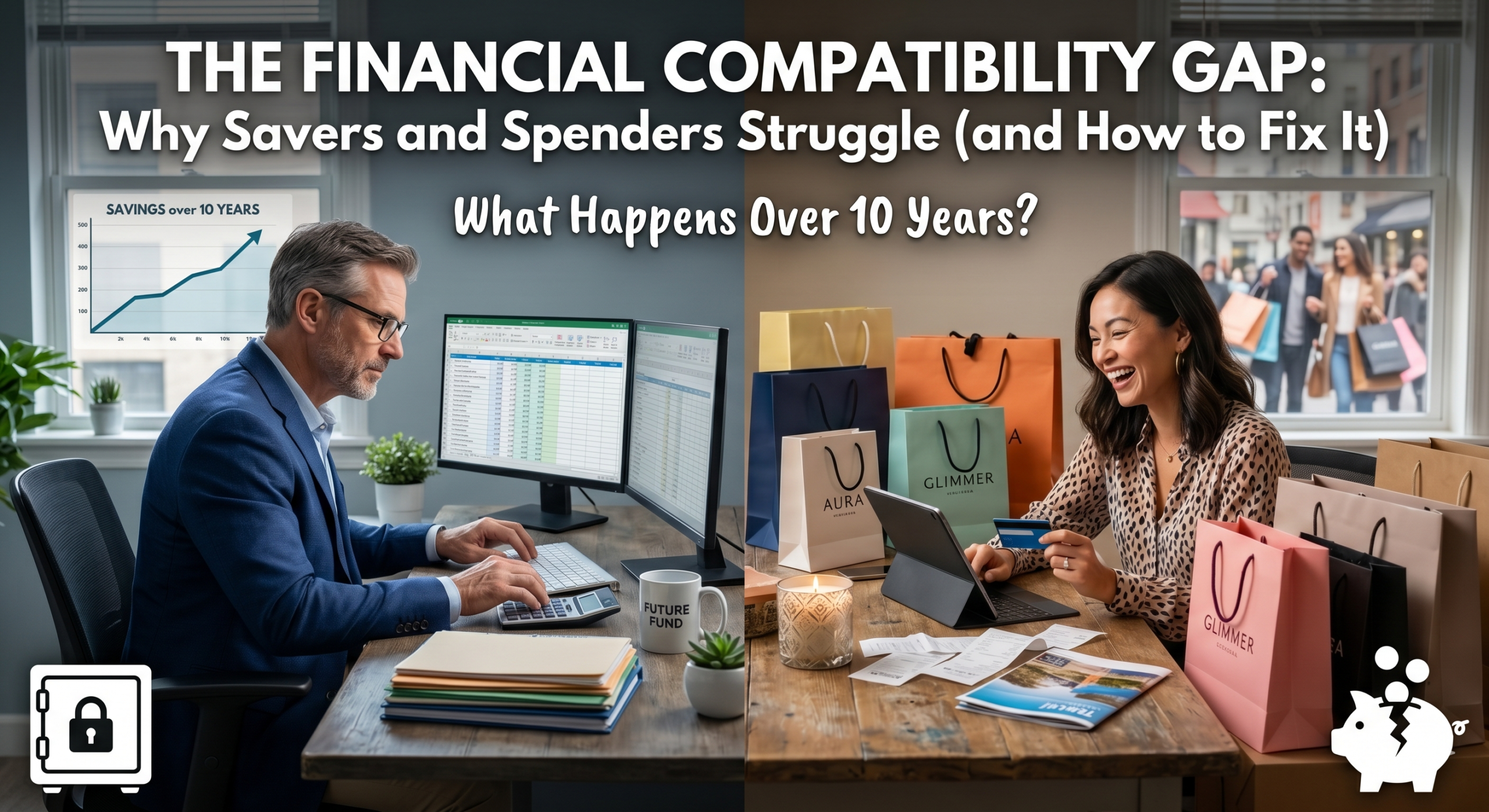

One Saver, One Spender: What Happens Over 10 Years?

We have all heard the old trope that “opposites attract”. The steady, spreadsheet-loving “Saver” meets the magnetic, life-of-the-party “Spender,” and we are told they will balance each other out like some financial yin and yang. It is a classic rom-com setup: the wealthy, rigid hero falls for the impulsive free spirit who teaches them what really matters.

Has anyone in this relationship thought about financial compatibility?

Here is the unromantic truth: in the real world, “opposites attract” makes for great cinema but terrible joint tax returns. Without a shared framework and deep self-awareness, a Saver and a Spender do not usually “balance” each other; they enter a ten-year cycle of lecturing and hiding that ages a relationship faster than rust ages a car.

If you are currently sitting across the dinner table from someone whose financial habits make you want to scream—or if you are the one quietly hiding your recent Amazon receipts—this case study is for you. We are going to look at the ten-year trajectory of Marcus and Elena, a fictional couple who walked into marriage with high chemistry, mutual love, and a total lack of financial alignment.

Phase 1: The Honeymoon and the “Renovation Fantasy”

Marcus and Elena met at 25. Both were ambitious, had the same degree, and started with identical salaries. On paper, they were indistinguishable. However, their “Money DNA” could not have been more different.

Marcus is a classic Saver. He is “Vigilant” to the core, checking his bank apps with the same mild curiosity others use to check the weather. He grew up watching his parents argue about late bills, and he decided early on that he would never be in that position. To Marcus, a rising savings balance is not just a number; it is a “satisfied chill” that represents protection against a world that might try to take things away.

Elena is a Spender. She is the first to pick up the check and the one who knows exactly which restaurants are worth the drive. To her, money is “weather”—it is something that comes and goes, and its primary purpose is to make life feel rich, social, and vibrant. She is not “broke,” but her closet definitely does not match her retirement account.

When they got married at age 28, they both fell for the “Renovation Fantasy”.

- Marcus’s Fantasy: “Once we settle down, she will see how much better it feels to have a six-month emergency fund. I will teach her the beauty of the spreadsheet”.

- Elena’s Fantasy: “He is so stable, which is great, but he is a little joyless about money. Once we are married, I will help him loosen up and actually enjoy the life he is working so hard for”.

They did not have the “Current State of the Union” conversation because it felt “rude,” “unromantic,” or “shallow”. Instead, they merged their lives based on chemistry and “biological fog,” assuming their love would naturally iron out the details.

Phase 2: The 5-Year Drift and the “Lecture-and-Hide” Cycle

Fast forward five years to age 33. The “chemical state” of early love has burned off, as it usually does within the 18-to-36-month window of a relationship. Marcus and Elena are now living in their “sober selves,” and the financial friction is no longer a cute quirk—it has become the relationship’s permanent background hum.

Because they chose a “Fully Joint” account model without establishing personal autonomy, every transaction is visible to both. This creates a “surveillance” dynamic that erodes trust.

- Marcus sees the $85 boutique candle.

- He sees the third Target run of the week.

- He sees the “small” daily lunch dates that add up to hundreds of dollars a month.

Marcus responds by lecturing. He brings up the long-term math, the “opportunity cost” of her spending, and the “Hidden Math of Love”. He acts like the household CEO because he is the only one “paying attention”.

Elena responds by hiding. She starts keeping a separate credit card Marcus does not know about—a form of “financial infidelity”. She leaves shopping bags in the trunk of the car until he is in bed. She is not being “malicious”; she is practicing a defense mechanism to avoid the pain of being judged or “accounted for” by her partner.

This is the “Lecture-and-Hide” cycle in action. Instead of the “Dual-Income Wealth Multiplier,” where sharing fixed costs triples their capacity to save, they are “treading water in a fancier pool”. Elena’s spending has scaled exactly with their raises, a phenomenon known as lifestyle inflation.

Phase 3: Year 10 — The “Combustion” Point

By Year 10, Marcus and Elena are 38. On paper, they look like the “power couple”. They have a suburban home, two late-model SUVs, and a vacation history that looks great on social media. But behind the facade, they are financially fragile.

Then, life does what life does: the economy shifts, and Marcus’s company goes through a “restructuring”. He is laid off.

In a healthy partnership, this would be a “yellow light”—a moment to sit down, run the numbers, identify what is controllable, and start working the problem together. But because Marcus and Elena have lived as “opposites” rather than “allies,” the job loss triggers a combustion:

- The Absence of a Foundation: They have no Emergency Fund because every “extra” dollar over the last decade went toward maintaining the “Status” lifestyle Elena craved and Marcus eventually subsidized through his avoidance of conflict.

- The Discovery: During the crisis, Marcus discovers the secret $12,000 credit card debt Elena has been carrying.

- The Divorce Penalty: The resentment peaks. Marcus feels he has been “playing defense” his whole life while his partner played “offense” against their own future. If they divorce now, the typical process will erase roughly a full decade of wealth-building progress for both of them.

The gap between their current reality and where they could have been—had they partnered with a “Conscientious” co-pilot—is now measured in the millions of dollars.

Phase 4: The Pivot — How to Save the Next 10 Years

If you see your own relationship in Marcus and Elena’s story, do not panic. Personality types are not destiny; they are just strong currents. You can swim against them with effort and awareness. You cannot “renovate” your partner, but you can change the architecture of your financial life.

To move from “Opposites” to “Allies,” Marcus and Elena must implement three structural changes:

1. Move to the “Yours, Mine, Ours” Model

The “Fully Joint” model was poisoning them because Marcus felt like a jailer and Elena felt like a child. They need a Hybrid Architecture:

- Ours: A joint account for rent, groceries, and shared savings goals.

- Yours & Mine: Personal accounts for discretionary spending. Marcus does not get to have an opinion on what Elena buys from her personal account, and Elena no longer feels the need to hide her shopping bags.

2. Proportional Contributions

If Marcus earns $120,000 and Elena earns $60,000, an “equal” 50/50 split of bills is quietly punishing Elena. They should switch to proportional contribution. Marcus pays 67% of the joint expenses, and Elena pays 33%. This ensures both partners have the same percentage of their income left for personal use, restoring a sense of fairness to the partnership.

3. The Monthly “Money Date”

They must replace the “annual tax-time fight” with a Money Date:

- 30 to 60 minutes once a month.

- Wins first: “We hit our savings goal for the emergency fund!”.

- Decisions next: “Do we need to adjust our travel budget for next year?”. This ritual turns money from a “catastrophic event” into simple “household maintenance”.

The Red Flags Most Savers Miss

In the early years, Marcus (our Saver) saw Elena’s spending as a “personality trait”—a zest for life that he lacked. He was blinded by “biological fog,” the chemical state where the brain’s prefrontal cortex (responsible for risk assessment) is effectively suppressed. If he had been looking with “both eyes open,” he would have noticed the whispering red flags that predict financial disaster:

- Lifestyle That Doesn’t Match Earnings: Elena’s apartment and wardrobe were funded by a “generous parent” or revolving credit, rather than her actual paycheck.

- Constant Small Emergencies: There was always a “car repair” or a “broken phone” that required Marcus to “spot her”—a pattern that signals an absence of a financial system.

- Vagueness as a Strategy: When Marcus asked concrete questions about her savings, Elena would respond with, “I’m doing okay” or “I’ve got some money set aside,” which is a classic evasion tactic.

- The “I Don’t Do Money Stuff” Identity: Elena wore her financial avoidance as a badge of honor, unconsciously expecting Marcus to handle the “adulting” for both of them.

Marcus assumed these things would change after marriage, but “renovating” a person is one of the most expensive lies we tell ourselves. Adults change when they hit a breaking point, not because they fell in love.

The Overlooked Green Flags of a Spender

It is easy to paint Elena as the “villain” in a wealth-building story, but that is a one-sided view. A partnership with a Saver who has turned into a “hoarder” can be just as joyless. Spenders bring vital Green Flags that Savers often lack:

- Social Charisma & Generosity: Spenders like Elena often build the deep networks that lead to career opportunities and “raises”.

- A “Living” Focus: They prevent the household from falling into “joyless accumulation,” ensuring that vacations are taken and memories are made.

- The Pivot Potential: If a Spender is “Conscientious”—meaning they return texts, show up on time, and follow through—they can be trained into a system.

The goal for this couple was never to turn Elena into Marcus; it was to find the “Shared Values” beneath their different habits.

The 12 Questions That Could Have Saved Them

If Marcus and Elena had sat down during that “Starting to Feel Real” window (around month six), they could have used the 12 Questions to Ask Before Commitment to surface these mismatches early:

- “What was money like in your family growing up?” This would have revealed Marcus’s “Vigilance” and Elena’s “Money Worship” scripts, helping them understand why they react the way they do.

- “What is your total debt right now—all of it?” This forces the “secret” credit cards into the light before the wedding planning begins.

- “What is your honest 10-year vision for your life?” Marcus might have said “Financial Independence at 50,” while Elena said “A beach house and luxury travel now”. Chemistry cannot fix a diverging vision; only negotiation can.

- “How do you feel about joint vs. separate finances?” They would have discovered early that “Fully Joint” was a recipe for surveillance and resentment, allowing them to build the “Yours, Mine, Ours” architecture from Day One.

The “Sober Self” and the Long Game

Ten years in, Marcus and Elena have to face their “Sober Selves”—the everyday, unremarkable version of who they are when the butterflies are gone. Marcus is not a “boring accountant”; he is a reliable co-pilot. Elena is not a “reckless shopper”; she is the engine of the family’s social life.

The difference between a couple that “combusts” and a couple that “multiplies” is Trust. A partner you trust adds capacity to your life; a partner you have to “manage” or “hide from” burns cycles you could be using to build your career.

The Transformation Checklist:

- Stop the “Renovation Fantasy”: Accept who your partner is today.

- Build the “Legal Architecture”: If you are 10 years in, you need a Postnup or updated Wills to protect what you have managed to save.

- Have the “Hard Conversation”: The one you have been avoiding is the one that will do the most work for your future.

Conclusion: Romance is Honesty

We are told that real love “transcends” money, but the couples who refuse to look at the math aren’t more romantic—they’re just more vulnerable. Marcus and Elena spent a decade in a “Lecture-and-Hide” cycle because they were afraid that being honest would be “unromantic”.

The truth is that “Boring is Beautiful.” Reliability, conscientiousness, and a 30-minute monthly Money Date are the ingredients of a love that actually lasts. If you want your partnership to survive the things that break most loves, you have to choose to love with “both eyes open.”

Your partner is the most important financial decision you will ever make. You can either be Jordan and Avery—building a quiet, steady life that compounds into $2 million—or you can be Sam and Riley, whose “opposite” habits create a gap larger than most people earn in their entire careers.

In the next 7 days, take one action: Pull your credit report, check your beneficiaries, or simply ask your partner: “What did money feel like in your house when you were eight?”. The trajectory of your next ten years starts with that one choice.