So, your partner just got laid off. Or maybe it was you. Either way, somebody in your household is now home full-time staring at the ceiling, watching the savings account shrink, and wondering how you’re supposed to pay for Netflix AND groceries.

First things first — breathe. You’re not the first couple to go through this, and you won’t be the last. But here’s the thing nobody tells you before it happens: losing one income in a two-income household isn’t just half the financial problem. It somehow feels like ten times the financial problem. And the emotional weight that comes along with it? That’s basically free of charge. Lucky you.

Let’s talk about what actually happens — financially, emotionally, and practically — when one partner in a relationship suddenly finds themselves without a paycheck.

The First 48 Hours: Financial Whiplash Is Real

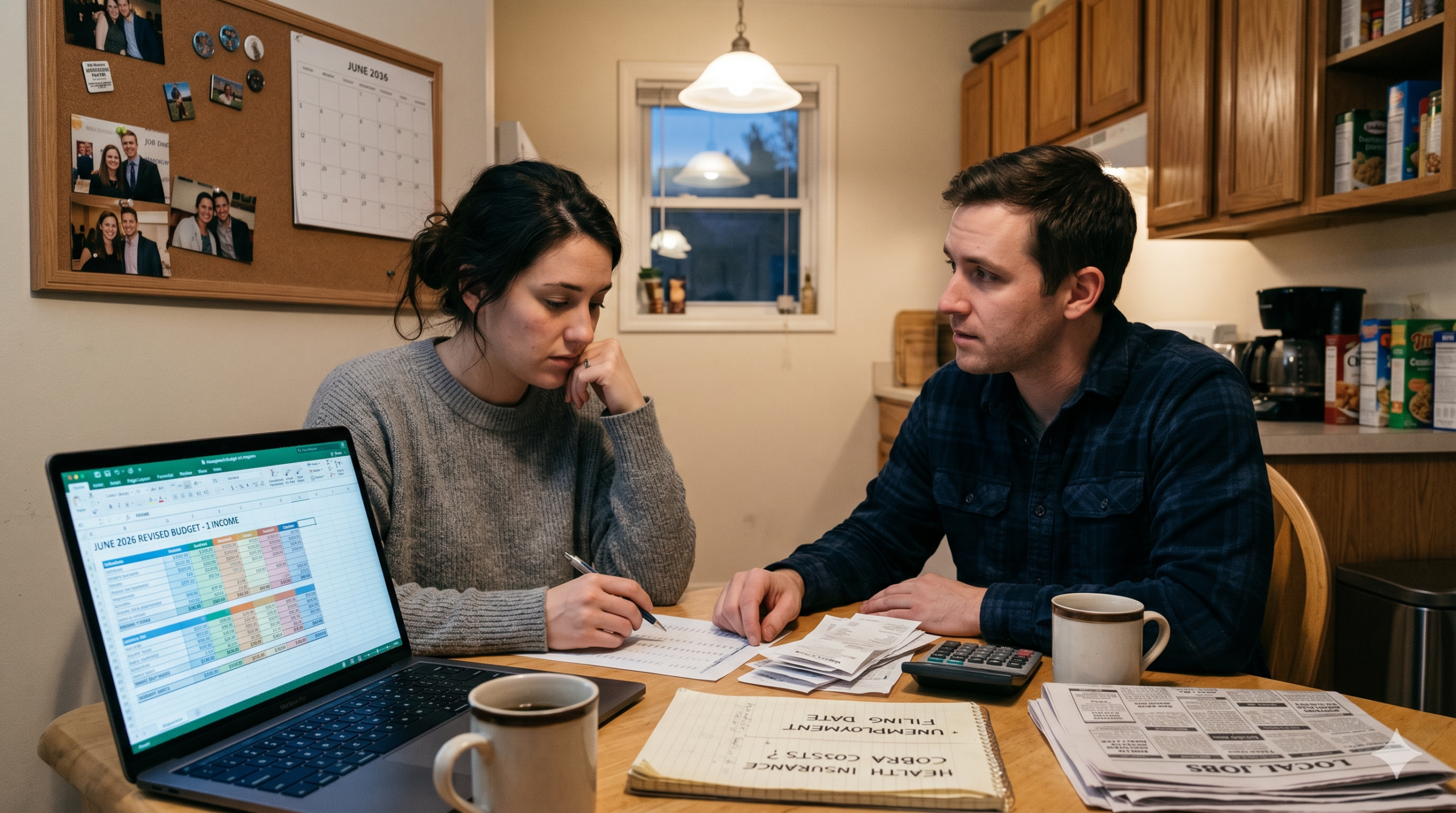

The moment one partner loses their job, your household budget just got flipped upside down and shaken like a snow globe. Everything you thought you knew about your monthly expenses is now up for review.

Here’s the thing about money — it doesn’t care about your feelings. The mortgage is still due on the 1st. The car payment doesn’t know your partner got laid off. The electric company is not going to send a “thinking of you” card and give you a month off.

In those first 48 hours, you’re going to have two very different instincts: panic or denial. Some couples immediately sit down, open every bank statement, and start calculating how long they can survive. Other couples order pizza, binge something on TV, and quietly agree not to talk about it for a few days. Both are very human responses. But only one of them is helpful.

The smart move is to do a quick financial triage. That means pulling up your bank accounts, knowing exactly what’s coming in (now just one salary, probably), and lining it up against what’s going out. Just the basics: rent or mortgage, utilities, food, car, insurance, minimum debt payments. Everything else — the gym membership, the subscription boxes, the three streaming services — those are conversations for day two.

The Income Gap: More Than Just the Missing Paycheck

Here’s what a lot of couples don’t realize until they’re in the thick of it: it’s not just the salary you lose. When one partner stops working, there’s a whole pile of financial losses that come with it.

Health insurance is a big one. If the partner who lost their job was the one carrying the family health insurance through their employer, you’re now looking at either switching to the other partner’s plan, paying for COBRA (which is famously expensive — we’re talking hundreds of dollars a month), or shopping the marketplace. Either way, that’s a new cost that just appeared out of nowhere.

Retirement contributions take a hit too. If your partner was contributing to a 401(k), that stops. And if their employer was matching those contributions, you’ve now lost free money on top of lost income. Yes, free money — gone. Pour one out.

Work-related tax deductions and employee benefits — think life insurance, FSAs, commuter benefits, tuition reimbursement — all those little perks disappear overnight. You don’t always notice how much those things add up until they’re gone.

Then there’s the less obvious stuff. Some people spend money because of work — lunches out, dry cleaning, gas, parking, professional memberships. When those go away, it saves a little money. But they’re nowhere near enough to offset the missing income.

Unemployment Benefits: Yes, File. No, It Won’t Cover Everything.

If your partner lost their job through no fault of their own — meaning a layoff, not a quit or a firing for cause — they should file for unemployment benefits immediately. Do it the same week. Don’t wait.

Unemployment benefits vary a lot by state, but they typically replace somewhere between 40% to 50% of your previous wages, up to a state-set maximum. That sounds decent until you realize that maximum in many states caps out at somewhere between $300 and $600 per week. If your partner was making $60,000 a year, that’s about $1,150 a week before taxes. Unemployment might cover $400 to $500 of that. The other $650 to $750? That’s your problem now.

Also — and this is important — unemployment benefits don’t last forever. Depending on your state, you’re typically looking at 12 to 26 weeks of benefits. If your partner’s job search runs longer than that, you’re back to zero income from that side.

So yes, file immediately. Get every dollar you’re entitled to. But don’t build your budget around it as if it’s a full replacement salary, because it isn’t even close.

Renegotiating Your Budget: The Talk Nobody Wants to Have

At some point — ideally sooner rather than later — you two need to sit down and have the money talk. Not the blame talk, not the “I told you so” talk, and definitely not the “let’s just see what happens” talk. The actual, real, honest-to-goodness money conversation.

This means writing down every single monthly expense. Not the vague number you think you spend — the real number. If you genuinely have no idea what you spend on groceries because you’ve just been swiping the card for years, now is the time to find out. (Spoiler alert: it’s probably more than you think.)

Once everything’s on the table, you categorize it:

Fixed expenses — the things you can’t easily change in the short term. Rent or mortgage, car payments, insurance, minimum loan payments. These are your non-negotiables.

Semi-fixed expenses — things you technically need but have some control over. Groceries, utilities, gas. You can’t eliminate them, but you can reduce them.

Discretionary expenses — dining out, subscriptions, entertainment, hobbies, Amazon impulse buys at 11pm. These are your first targets.

The goal isn’t to make life miserable. The goal is to stretch your runway — meaning, how long can you live on the one income (plus any savings and unemployment) while your partner finds new work? Give yourselves a realistic number. If you can survive six months without draining savings completely, that’s a very different situation than if you’re out of money in 45 days.

Emergency Fund Reality Check

This is where couples really feel whether they made the right financial decisions before this happened. If you have three to six months of living expenses saved in an emergency fund, congratulations — you are better prepared than a large portion of the population, and this situation is painful but survivable without catastrophic damage.

If your emergency fund is approximately zero dollars? Well, welcome to the club that nobody wanted to join. You’re not alone — a shocking number of households have little to nothing saved for emergencies — but you are in a tighter spot and need to act faster.

With no emergency savings, one income has to stretch to cover everything. That might mean tapping into other accounts — a savings account, a brokerage account, even asking about hardship withdrawals from retirement accounts (though that comes with penalties and taxes, so it’s a last resort, not a first move).

If you end up needing to pull from a 401(k) before age 59½, you’re generally looking at a 10% early withdrawal penalty plus ordinary income taxes on the money. So if you pull out $10,000, you might only net $7,000 to $7,500 after the penalty and taxes. That’s a very expensive emergency fund to crack open.

Debt Doesn’t Take a Vacation

This is the part where couples with existing debt really start to feel the squeeze. Car loans, student loans, credit card balances, personal loans — none of those lenders got the memo about the job loss. They just keep sending statements.

If money is truly tight, the first calls you make should be to your creditors. Yes, actually pick up the phone and call. Many lenders — especially federal student loan servicers, mortgage companies, and credit card companies — have hardship programs. These might include:

- Temporarily reduced or paused payments

- Waived late fees during hardship periods

- Extended payment terms to lower monthly minimums

- Interest-only payment periods

They don’t advertise these options loudly, but they exist. The worst thing you can do is just stop paying without saying anything, because that leads to late fees, credit score damage, and eventually collections — which makes a hard situation much harder.

Mortgage companies in particular are required to offer certain loss mitigation options under federal rules. If you have a federally backed mortgage and you’re struggling, look into forbearance — it’s a temporary pause on payments that buys you time without wrecking your credit.

The One-Income Household Math

Let’s talk about what your budget might actually look like when you go from two incomes to one. This is going to be different for every couple, but here’s a simple example to illustrate the point.

Say your household was bringing in $8,000 a month after taxes between both partners — $5,000 from one and $3,000 from the other. Your expenses were running about $6,500 a month, and you were saving or spending the other $1,500 with some breathing room.

Now one of those incomes disappears. Suddenly you’re at $5,000 a month in income versus $6,500 in expenses. That’s a $1,500 monthly deficit. Every month you don’t fix that, you’re either draining savings or going into debt. And unemployment might cover $1,500 to $2,000 a month, but remember — that’s temporary.

The math only works if you either increase income (side gigs, freelance work, the employed partner picking up extra shifts) or decrease expenses (cutting the budget down from $6,500 closer to $4,500 or $5,000), or both. There’s no magic third option, even though it would be great if there were.

How This Stress Affects the Relationship — and Why It Matters Financially

Okay, so this is a financial relationship site, and we need to talk about something that sounds soft but actually has very real financial consequences: the emotional and relational fallout of job loss.

When one partner loses their job, both people feel it — just differently. The unemployed partner often feels shame, anxiety, and a loss of identity (especially if their career was a big part of who they are). The employed partner may feel resentment, fear, and pressure — even if they’d never say it out loud. These emotions, when left unaddressed, can lead to arguments about money, which research consistently shows is one of the top reasons couples fight and split up.

And breakups or divorces? Extraordinarily expensive. We’re talking legal fees, splitting assets, potentially two separate households, and all the financial decisions that have to be unwound. The cost of relationship dysfunction that started with a job loss can far exceed the financial loss of the job itself.

That’s not a reason to stay in a relationship that isn’t working. But it is a reason to take the emotional side of this seriously — to communicate, check in with each other, and maybe talk to a couples counselor if the tension gets heavy. Therapy is a lot cheaper than a divorce lawyer. Just saying.

Roles Can Shift — and That Has Financial Consequences Too

Something interesting happens when one partner loses their job: suddenly the household dynamics shift. The employed partner becomes the sole breadwinner. The unemployed partner often takes on more domestic responsibilities — more cooking, cleaning, handling errands.

For some couples, this works fine temporarily. For others, it creates new tension. The employed partner may start feeling like they’re carrying everything financially while also being expected to pull equal weight at home. The unemployed partner may feel like they’ve lost their power in the relationship along with their paycheck.

These dynamics have financial consequences. They affect whether big purchases get approved by both partners equally, who controls the budget, and whether the unemployed partner keeps pushing hard on the job search or starts getting comfortable with the arrangement. None of these are small things.

The key is to establish expectations early. Have the conversation: what’s the timeline expectation for finding new work? What’s each person’s role during this period? How are decisions being made? Getting this stuff on the table keeps resentment from quietly compounding like interest on a credit card.

The Job Search Has Costs Too

Here’s something people forget: looking for a new job costs money. Not a huge amount, but more than zero.

There’s the professional wardrobe update for interviews. The resume service, if you use one. LinkedIn Premium, which your partner may feel pressured to subscribe to. Gas or rideshare costs for in-person interviews. And if they’re changing industries, there may be certification courses or continuing education involved.

None of these are outrageous individually, but together they can add up to a few hundred dollars that you weren’t expecting to spend. Budget for the job search itself so it doesn’t blindside you.

When to Tap Savings (and When Not To)

This is one of the most common questions couples face: should we dip into savings while we look for work, or try to avoid it?

The general answer is: yes, that’s what savings are for. But there’s a smart way to do it and a panicked way to do it.

The smart way is to calculate your monthly shortfall (expenses minus income), figure out how many months your savings can cover that gap, and set a decision point. For example, if your savings can cover the shortfall for four months, decide now that if your partner hasn’t found work in three months, you’re going to start evaluating more drastic options — selling a car, moving to a cheaper place, one of you picking up a second job.

The panicked way is to just drain savings month by month without a plan, hoping things work out, until one day you’re looking at a bank account with $400 in it wondering how it happened. (It happened because there was no plan. The bank account knew. It tried to warn you.)

What If It Goes Long-Term?

Most job searches resolve in a few weeks to a few months. But some stretch longer — especially in competitive fields, during economic downturns, or for workers in industries that are shrinking. If you’re heading past the six-month mark without a new job, you need to reassess your situation more seriously.

Long-term strategies might include:

Relocating. Sometimes the jobs are elsewhere, and staying in the same city because it’s comfortable is costing you more than a move would.

Changing industries or roles. If the field your partner left is laying people off left and right, pivoting to an adjacent industry with better prospects may be the move.

One partner taking on more income. The employed partner picks up overtime, a side job, or a freelance gig to help close the gap.

Downsizing. Moving to a less expensive home or apartment is a big step, but it can dramatically reduce your monthly burn rate and give you more runway.

The partner returning to school or retraining. Some job losses are a signal from the universe (or the economy) that a career change is coming whether you like it or not. Retraining programs — especially community college, trade programs, and certifications — can be completed relatively quickly and affordably.

Coming Out the Other Side

Here’s the thing that couples who survive job loss well have in common: they treat it as a team problem, not one person’s failure. They communicate about money openly and honestly, they adjust their lifestyle without making each other feel guilty, and they keep their eyes on the future instead of drowning in the present moment.

Job loss is a financial crisis, yes. But it’s also an opportunity — weird as that sounds — to get honest about your finances, build better habits, and come out the other side with a clearer picture of what your household actually needs versus what it just got used to having.

The couples who come out stronger from something like this are the ones who faced it together instead of letting it drive a wedge between them. And when the next paycheck comes — and it will — you’ll have something most couples never get: a real, tested understanding of how you handle hard times together.

That’s worth more than the job that was lost.

Quick Recap: What to Do Right Now

If you’re in this situation today, here’s your short action list:

Day 1: Pull up your bank accounts and know your exact numbers.

Day 1-3: File for unemployment benefits immediately if your partner qualifies.

First week: Write down every monthly expense — fixed, semi-fixed, and discretionary.

First week: Contact any creditors where you’re at risk of missing payments and ask about hardship programs.

Ongoing: Set a timeline for the job search and check in on it regularly as a couple.

If it goes long: Revisit housing, transportation, and income options honestly and without blame.

You can get through this. It’s not easy, but it’s survivable — especially if you face it together instead of pretending it’s not happening.